Choosing the right health insurance plan in the United States can feel overwhelming—especially when comparing HMO, PPO, and EPO plans. These are the most common types of managed care health insurance options, and each comes with different rules, costs, and levels of flexibility.

Understanding the differences between these plans is essential for making informed healthcare decisions that fit your budget, lifestyle, and medical needs.

In this comprehensive guide, we’ll break down HMO vs PPO vs EPO, including how they work, their pros and cons, and which one might be best for you.

What Are HMO, PPO, and EPO Plans?

Health insurance plans in the U.S. are often structured around provider networks—groups of doctors, hospitals, and specialists that agree to provide care at negotiated rates.

HMO (Health Maintenance Organization)

An HMO plan requires members to use a network of providers and select a Primary Care Physician (PCP) who coordinates all care.

PPO (Preferred Provider Organization)

A PPO plan offers the most flexibility, allowing members to visit both in-network and out-of-network providers without referrals.

EPO (Exclusive Provider Organization)

An EPO plan is a hybrid option that offers no referral requirements but limits coverage strictly to in-network providers.

Key Differences: HMO vs PPO vs EPO

| Feature | HMO | PPO | EPO |

|---|---|---|---|

| Primary Care Physician (PCP) | Required | Not required | Usually not required |

| Specialist Referrals | Required | Not required | Not required |

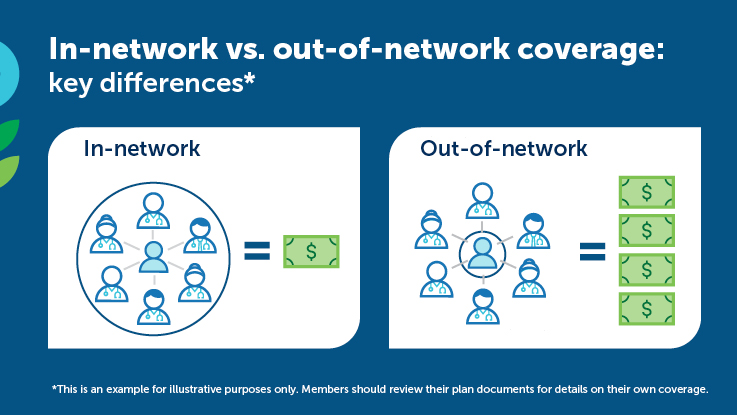

| Network Restrictions | In-network only | In & out-of-network | In-network only |

| Out-of-Network Coverage | No (except emergencies) | Yes (higher cost) | No (except emergencies) |

| Monthly Premium | Low | High | Moderate |

| Flexibility | Low | High | Medium |

HMO Plans: Affordable but Structured

How HMO Works

- You must choose a Primary Care Physician (PCP)

- Referrals are required to see specialists

- Care is covered only within the network

Advantages

- Lower monthly premiums

- Lower out-of-pocket costs

- Coordinated and centralized care

Disadvantages

- Limited provider choices

- Less flexibility

- No coverage outside the network

👉 Best for: Individuals or families who want cost-effective coverage and structured care management

PPO Plans: Maximum Flexibility

How PPO Works

- No need for a primary care physician

- No referrals required

- Access to both in-network and out-of-network providers

Advantages

- Greater freedom in choosing doctors

- No referral requirements

- Ideal for people who travel frequently

Disadvantages

- Higher premiums

- Higher deductibles and out-of-pocket costs

👉 Best for: Individuals who value flexibility and wider provider access

EPO Plans: A Balanced Middle Option

How EPO Works

- No referrals required

- Must use in-network providers

- No out-of-network coverage except emergencies

Advantages

- Lower cost than PPO

- More flexibility than HMO

- Simple structure without referrals

Disadvantages

- Limited to network providers

- No coverage outside the network

👉 Best for: Individuals who want a balance between affordability and flexibility

Factors to Consider When Choosing a Plan

Selecting the right plan depends on several personal factors:

1. Budget

- HMO: Lowest cost

- EPO: Moderate cost

- PPO: Highest cost

2. Doctor Preference

- If you want to keep your current doctor, check if they are in-network

3. Flexibility Needs

- Frequent travelers or people needing specialists may prefer PPO

4. Health Conditions

- Chronic conditions may require more flexibility and specialist access

Real-Life Scenarios

- Young, healthy individuals: Often choose HMO for affordability

- Frequent travelers or professionals: Prefer PPO for flexibility

- Families: May choose EPO for balanced cost and access

Understanding the differences between HMO, PPO, and EPO health insurance plans is crucial for making informed decisions in the U.S. healthcare system.

- HMO: Best for affordability and structured care

- PPO: Best for flexibility and provider choice

- EPO: Best for a balance between cost and convenience

The ideal plan depends on your healthcare needs, financial situation, and lifestyle preferences. Taking time to compare options can help you choose a plan that provides both financial protection and peace of mind.